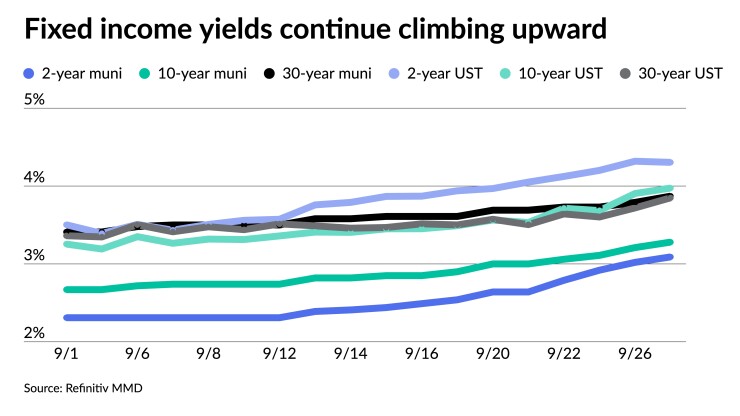

Municipal triple-A yield curves saw another round of cuts Tuesday amid elevated secondary selling pressure, pushing one-year munis to end the session above 3%. U.S. Treasuries and equities saw losses after more hawkish Fed speak and a continued global bond rout.

Triple-A yields rose by as many as seven to eight basis points across the curve, moving the entire triple-A curve above 3% and the 30-year a dozen basis points shy of 4%. UST saw larger losses out long.

Short ratios climbed Tuesday. The three-year was at 70%, the five-year was at 74%, the 10-year at 83% and the 30-year at 101%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the three at 70%, the five at 74%, the 10 at 86% and the 30 at 103% at a 4 p.m. read.

“Another day, another round of price cuts that have taken September’s yields from just long bonds trading with 3% handles to virtually nothing left in the 2% range (excluding some ultra-short names),” said Kim Olsan, senior vice president at FHN Financial.

And losses have stacked up with Bloomberg index data showing investment grades losing 3.3% in September and 11.64% year to date, high-yield 5.22% in the red for the month and 15.19% for 2022, taxable munis seeing 5% losses in September and 19.1% year to date while Bloomberg’s impact index has seen 4.09% losses in the month and 15.08% in 2022.

“Municipal yields are still higher and rising, propelled by the Fed’s fight with inflation and resulting fixed income fund outflows,” noted Municipal Market Analytics’ Partner Matt Fabian. “Value is now available for buyers capable of absorbing near-term losses.”

A series of weeks spent enduring daily price declines “has created opportunities along the entire curve,” Olsan said, noting that short-dated AAA- and AA-rated bonds trading between 3.00% and 3.25% now offer taxable equivalent yields 300 basis points or more from early-2022 levels.

In secondary trading Tuesday, one-year paper from Ohio, Washington, Denver and Boston, was all trading above 3%.

Long-term munis trading at yields more than 4.50% have seen TEYs jump to over 7% for a similar gain on a net basis, Olsan said.

“At these levels, high-grade munis have moved into a similar yield/return range of the S&P 500 over the last 20 years,” she said.

The market trend is telling, Olsan said. Noting that Monday’s trade volume via Municipal Securities Rulemaking Board data showed in very short maturities — 2023-2025 — dealer sells to customers were 56%-59%.

That ratio declined to 51% between 2029 and 2034 and long volume was at 50%-50% parity between dealer sells and buys to customers.

“This dynamic indicates more defensive posturing as the inflation/recession theme is played out,” she said. ”Heavy selling in short maturities (the most liquid and with smallest give up in yield) is playing into that demand while so much inquiry is left to decipher fair value.”

Olsan noted that premarketing wires for the upcoming Texas water revenue bond deal, long 4% coupon yields approach 5%.

“Down the credit curve, 5% coupon airport and hospital names have moved into discounted levels past 25 years — an indication that any further weakness will infiltrate high-grade 5s as well,” Olsan added.

While the front of the curve “are now plunged deeply into oversold valuations with negative momentum, longer maturity valuations actually strengthened a bit (versus the week before), allowing positive momentum that could benefit near-term buyers if the market at large at least holds it own,” Fabian said. “Sellers and issuers, on the other hand, may want to just wait a bit.”

In the primary market Tuesday, Piper Sandler & Co. preliminarily priced for San Antonio, Texas, (Aa2/AA+/AA/) $257 million of water system junior lien revenue bonds with 5s of 2023 at 3.06%, 5s of 2027 at 3.29%, 5s of 2032 at 3.56%, 5s of 2042 at 4.21%, and 5.25s of 2052 at 4.37%, callable 5/15/2032.

In the competitive market, Minnesota sold $332.350 million of state general fund appropriation refunding bonds to J.P. Morgan Securities LLC. Bonds in 3/2023 with a 5% coupon yield 3.03%, 5s of 2027 at 3.20% and 5s of 2030 at 3.32%, non call.

The City of County of Denver, Colorado, (Aaa/AAA//) sold $193.750 million of water revenue bonds to Morgan Stanley & Co. Bonds in 12/2023 with a 5% coupon yield 3.05%, 5s of 2027 at 3.17%, 5s of 2032 at 3.47%, 5s of 2037 at 3.76%, 4.375s of 2042 at 4.42%, 5s of 2047 at 4.25% and 5s of 2052 at 4.32%, callable 12/15/2032.

Secondary trading

Maryland 5s of 2023 at 2.98%. Boston 5s of 2023 at 3.01%-3.00%. Ohio 5s of 2023 at 3.15%. Washington 5s of 2023 at 3.24%-3.15%. Denver City and County 5s of 2023 at 3.11%-3.10%.

Utah 5s of 2025 at 3.12%. Minnesota 5s of 2025 at 3.25%-3.21%. North Carolina 5s of 2026 at 3.06% (2.92% Friday and 2.72%-2.69% Wednesday). Wisconsin 5s of 2027 at 3.24%-3.22%.

New York Dorm PITs 5s of 2030 at 3.50%-3.48%. California 5s of 2030 at 3.38%. New York City waters 5s of 2031 at 3.42%. Washington 5s of 2032 at 3.44%. New York City TFA 5s of 2033 at 3.65%-3.64% (3.17%-3.16% Thursday).

Washington 5s of 2039 at 4.01%-3.95%. San Antonio, Texas, ISD 5s of 2041 at 4.02%-4.01% (Friday 3.97%-3.93%).

California 5s of 2052 at 4.21% (Friday 4.08%-4.07%).

AAA scales

Refinitiv MMD’s scale was cut seven to 8 basis points at a 3 p.m. read: the one-year at 3.04% (+7) and 3.09% (+7) in two years. The five-year at 3.12% (+7), the 10-year at 3.28% (+7) and the 30-year at 3.87% (+8).

The ICE AAA yield curve was cut two to seven basis points: 3.05% (+2) in 2023 and 3.07% (+2) in 2024. The five-year at 3.12% (+5), the 10-year was at 3.33% (+5) and the 30-year yield was at 3.86% (+7) at a 4 p.m. read.

The IHS Markit municipal curve was cut seven basis points: 3.01% (+7) in 2023 and 3.07% (+7) in 2024. The five-year was at 3.13% (+7), the 10-year was at 3.29% (+7) and the 30-year yield was at 3.88% (+7) at a 4 p.m. read.

Bloomberg BVAL was cut six to seven basis points: 3.01% (+6) in 2023 and 3.04% (+6) in 2024. The five-year at 3.09% (+7), the 10-year at 3.23% (+7) and the 30-year at 3.88% (+7) at 4 p.m.

Treasuries were mixed.

The two-year UST was yielding 4.304% (-5), the three-year was at 4.398% (-2), the five-year at 4.221% (+3), the seven-year 4.142% (+3), the 10-year yielding 3.972% (+4), the 20-year at 4.158% (+10) and the 30-year Treasury was yielding 3.851% (+11) at the close.

Primary to come:

The Texas Water Development Board (/AAA/AAA/) is set to price Wednesday $971.935 million of State Water Implementation Revenue Fund for Texas Master Trust revenue bonds, Series 2022, serials 2023-2033, terms 2034, 2035, 2036, 2037, 2038, 2039, 2040, 2041, 2042, 2047, 2052 and 2057. Citigroup Global Markets.

The California Earthquake Authority (//A-/A+/) is set to price Wednesday $500 million of taxable revenue bonds, Series 2022A. Goldman Sachs & Co.

The Cypress-Fairbanks Independent School District, Texas, (Aaa/AAA//) is set to price $221.640 million of unlimited tax school building bonds, Series 2022A, insured by Permanent School Fund Guarantee Program. Mesirow Financial.

The Sweetwater Union High School District, California, (A1//AA+/) is set to price Wednesday $212.479 million of dedicated unlimited ad valorem property tax general obligation bonds, consisting of $11.245 million of Election of 2006 Proposition O bonds, Series D-1, serials 2023-2031; $44.390 million of Election of 2006 Proposition O bonds, Series D-3, serials 2031-2047; $1.190 million of Election of 2006 Proposition O bonds, Series D-1, serials 2023; $182.9550 million of Election of 2018 Measure DD bonds, Series A-1, serials 2023-2025 and 2028-2042, terms 2047 and 2052; and Election of 2018 Measure DD bonds, Series A-2, serial 2023. Citigroup Global Markets Inc., New York

The Board of Regents of the Texas A&M University System (Aaa/AAA/AAA/) is set to price Wednesday $202.875 million of revenue financing system bonds, Series 2022, serials 2023-2042, terms 2047 and 2052. Siebert Williams Shank & Co.

The Lower Colorado River Authority (/A/A+/) is set to price Thursday $194.585 million of LCRA Transmission Services Corporation Project transmission contract refunding revenue bonds, Series 2022A. Morgan Stanley & Co.

The Tennessee Housing Development Agency (Aa1/AA+//) is set to price Thursday $185,050 million of non-AMT social residential finance program bonds, Issue 2022-3, serials 2023-2034, terms 2037, 2042, 2047 and 2053. Citigroup Global Markets.

The Florida Housing Finance Corp. (Aaa///) is set to price Wednesday $125 million of non-AMT social homeowner mortgage revenue bonds, 2022 Series 3, serials 2024-2034, terms 2037, 2042, 2047, 2053 and 2054. Citigroup Global Markets.

Competitive:

Illinois (Baa1/BBB+/BBB+/) is set to sell $175 million of taxable general obligation bonds, Series of October 2022A, at 10:45 a.m. eastern Wednesday.

The state is also set to sell $245 million of general obligation bonds, Series of October 2022B, at 11:15 a.m. Wednesday.

Additionally, the state is set to sell $280 million of general obligation bonds, Series of October 2022C, at 11:45 a.m. Wednesday.

New Mexico (Aa2/AA-//) is set to sell $288.780 million of severance tax bonds, Series 2022B, at 10:30 a.m. Wednesday.

The New York Urban Development Corp. is set to sell $1.443 billion of tax-exempt personal income tax revenue bonds in multiple series Thursday.